1031 Exchange

1031 REPLACEMENT PROPERTIES

- Defer 100% of capital gains taxes

- Greater buying power by applying funds that would have been paid to the IRS towards a new property

- Nationwide properties

- Freedom from property management

- Re-leverage your equity

- Ability to increase annual cash flow

- Smart wealth preservation strategy

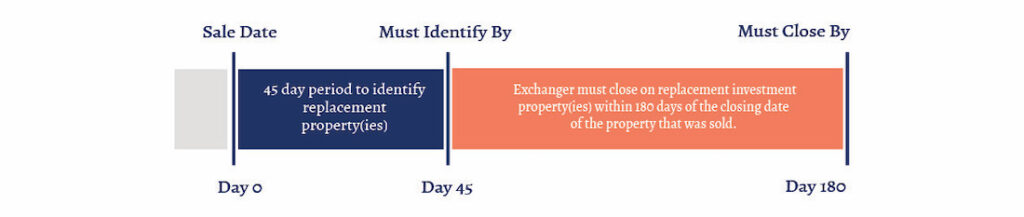

IS YOUR 45-DAY IDENTIFICATION PERIOD RUNNING OUT?

Cityside Capital works with savvy real estate investors to find replacement properties within the IRS guidelines to ensure continued deferral of your capital gains taxes. As licensed registered representatives, our broker dealer performs heavy due diligence on each property from our best in class multifamily and self-storage operators. We provide a proven solution to find a suitable replacement property with the right price tag, debt ratio, and closing schedule to meet your needs.

Schedule a Consultation

"*" indicates required fields

Definition of a 1031 Exchange

A 1031 exchange gets its name from Section 1031 of the U.S. Internal Revenue Code, which allows you to avoid paying capital gains taxes when you sell an investment property and reinvest the proceeds from the sale within certain time limits in a property or properties of like kind and equal or greater value.

In a 1031 Exchange, the IRS allows the owner of the property to sell one property and use the proceeds from the sale to buy another property without tax consequence – paying no capital gains taxes on the transaction. It’s one of the best methods for deferring the capital gains tax that ordinarily arises from the sale of real estate. The 1031 exchange provides real estate owners with greater leverage, increased diversification, increased potential for geographic relocation, improved cash flow, and an effective strategy for preserving wealth.

It’s important to note that in a 1031 transaction the capital gains taxes are deferred, not eliminated. When the replacement property is ultimately sold the original deferred gain and any additional gains on the replacement property will be subject to tax. The exception being if the replacement property is sold as part of another 1031 exchange. Taxpayers must report an exchange to the IRS on Form 8824, Like-Kind Exchanges and file it with their tax return for the year in which the exchange occurred. While 1031 exchanges require careful planning and close oversight, they can be a powerful tool to preserve an investor’s purchasing power.

The Role of Qualified Intermediaries

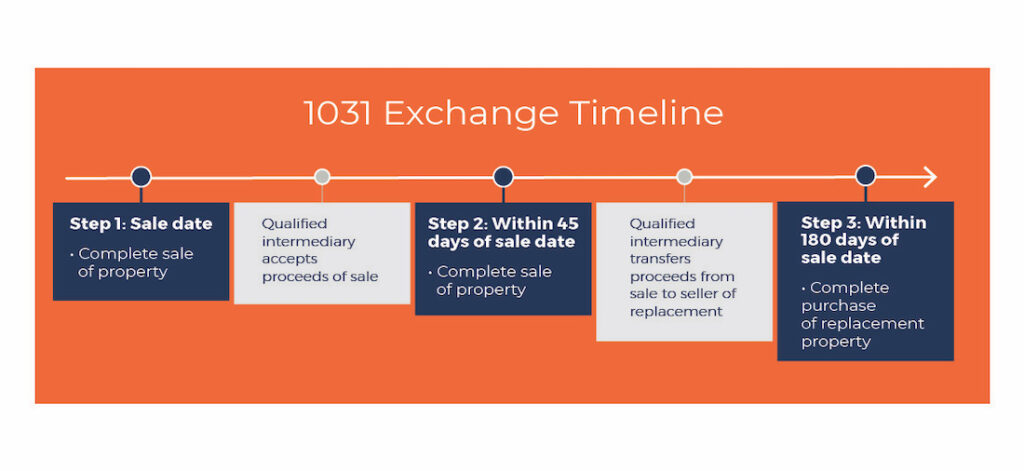

Under section 1031, any proceeds received from the sale of a property remain taxable. For that reason, proceeds from the sale must always be transferred to a qualified intermediary (“QI”), rather than the seller of the property, and the qualified intermediary transfers them to the seller of the replacement property or properties. A qualified intermediary is a person or company that agrees to facilitate the 1031 exchange by holding the funds involved in the transaction until they can be transferred to the seller of the replacement property. The qualified intermediary can have no other formal relationship with the party’s exchanging property.

What Is Depreciation and Why Is It Important to a 1031 Exchange?

Depreciation is an essential concept for understanding commercial real estate and one of the true benefits of a 1031 exchange.

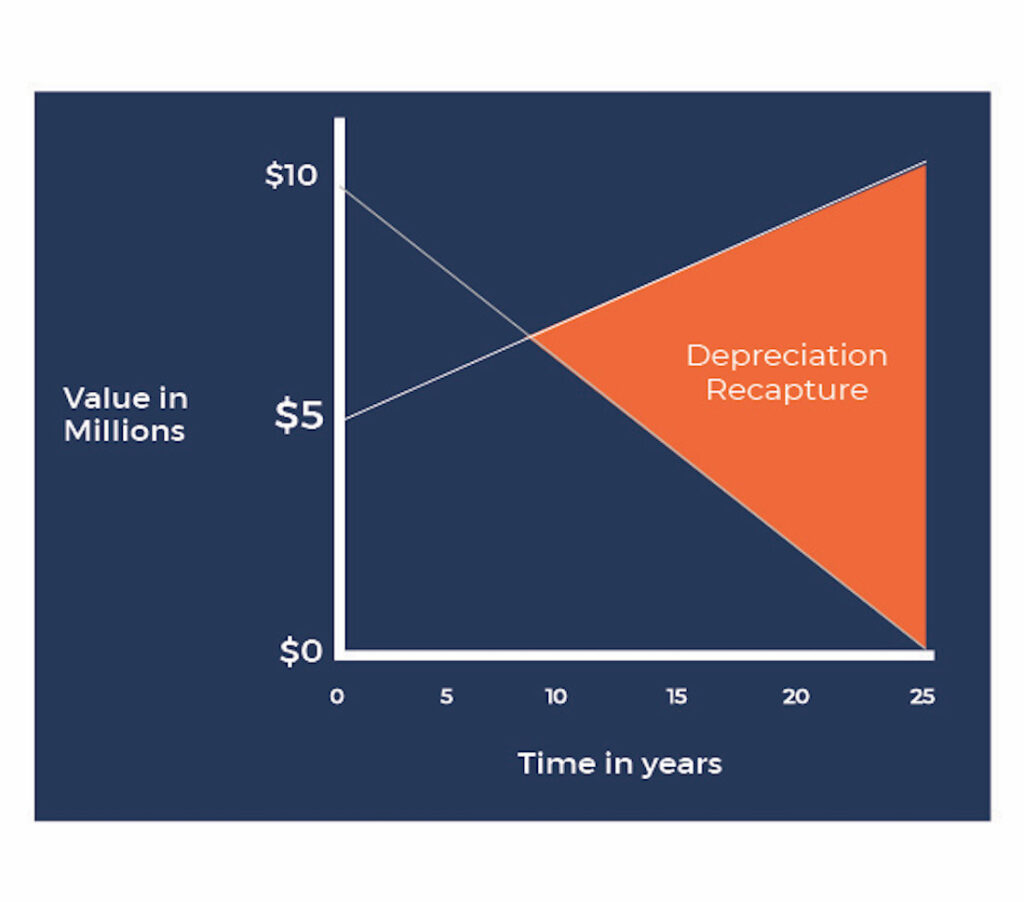

Depreciation is the percentage of the cost of an investment property that is written off every year, recognizing the effects of wear and tear. When a property is sold, capital gains taxes are calculated based on the property’s net-adjusted basis, which reflects the property’s original purchase price, plus capital improvements minus depreciation.

If a property sells for more than its depreciated value, you may have to recapture the depreciation. That means the amount of depreciation will be included in your taxable income from the sale of the property.

Since the size of the depreciation recaptured increases with time, you may be motivated to engage in a 1031 exchange to avoid the large increase in taxable income that depreciation recapture would cause when the property is sold. Depreciation recapture will be a factor to account for when calculating the value of any 1031 exchange transaction—it is only a matter of degree.

Choosing a Replacement Property: Timing and Rules

Like-kind property is defined according to its nature or characteristics, not its quality or grade. This means that there is a broad range of exchangeable real properties. Industrial property can be exchanged for a commercial building, for example, or multifamily can be exchanged for vacant land. But you can’t exchange real estate for cryptocurrency or artwork, for example, since that does not meet the definition of like-kind. The property cannot be for personal use and must be held for investment that typically implies a minimum of two years’ ownership.

In order receive the full benefit of a 1031 exchange, your replacement property should be of equal or greater value. You must identify a replacement property for the assets sold within 45 days and then conclude the exchange within 180 days.

There are three rules that can be applied to define identification. You need to meet one of the following:

1. The three-property rule – Identify three properties and acquire one or combination of the properties.

2. 200% rule – acquire up to 200% of the market value (less expenses) for any number of properties.

3. 95% rule – identify as many properties as you would like as long as you acquire properties valued at 95% of their total or more.

Tenant-In-Common Exchanges

Tenancy-in-common exchanges are another variation of 1031 transactions. Tenancy in common isn’t a joint venture or a partnership (which would not be allowed to engage in a 1031 exchange), but it is a relationship that allows you to have a fractional ownership interest directly in a large property, along with one to 34 more people/entities. This allows relatively small investors to participate in a transaction, as well as having a number of other applications in 1031 exchanges.

Strictly speaking, tenancy in common grants investors the ability to own a piece of real estate with other owners but to hold the same rights as a single owner. Tenants in common do not need permission from other tenants to buy or sell their share of the property, but they often must meet certain financial requirements to be “accredited.”

Tenancy in common can be used to divide or consolidate financial holdings, to diversify holdings, or gain a share in a much larger asset. It allows you to specify the volume of investment in a single project, which is important in a 1031 exchange, where the value of an asset has to be matched to that of another.

Estate Planning with 1031 Exchanges

One of the major benefits of participating in a 1031 exchange is that you can take that tax deferment with you to the grave. If your heirs inherit property received through a 1031 exchange, its value is “stepped up” to fair market, which wipes out the tax deferment debt.

This means that if you die without having sold the property obtained through a 1031 exchange, the heirs receive it at the stepped-up market rate value, and all deferred taxes are erased. An estate planner should be consulted to take maximum advantage of this opportunity. Tenancy in common can be used to structure assets in accordance with your wishes for their distribution after death.